Northeast Florida Housing Market Update — November 2025

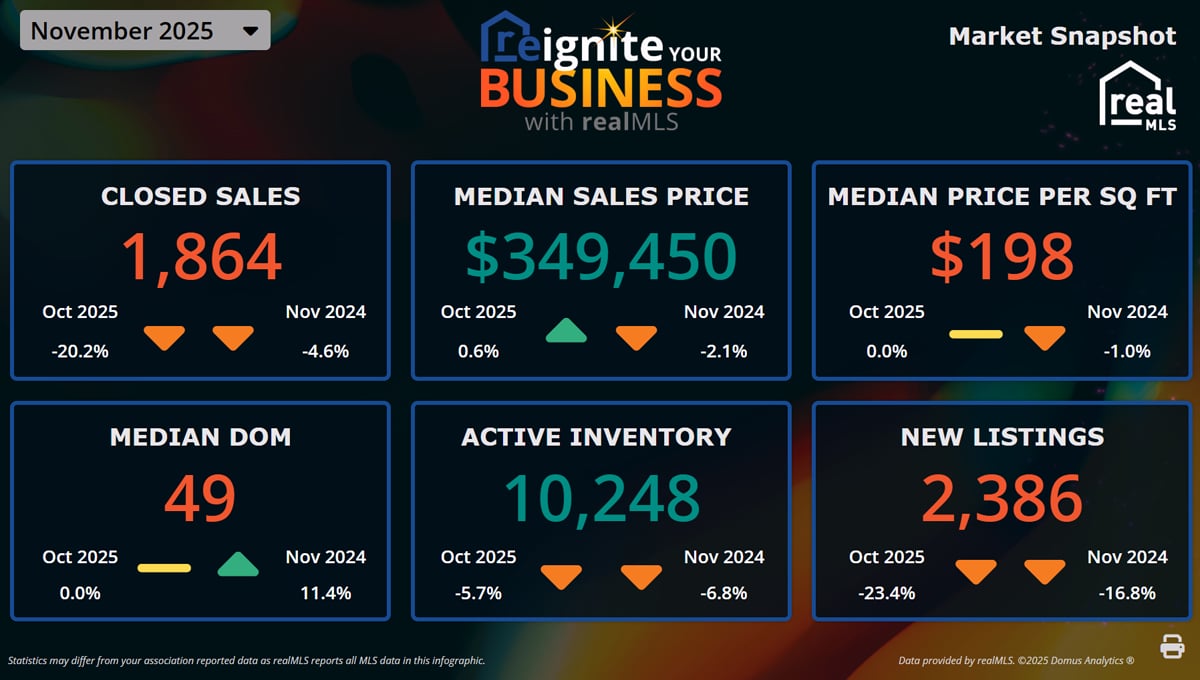

The November 2025 housing market showed a noticeable seasonal slowdown, with both buyer activity and new inventory pulling back as we moved into the holiday months.

Closed sales dropped to 1,864, which is a 20.2% decrease from October and 4.6% lower than November 2024. Fewer buyers stepped into the market this month, which is typical for late fall.

Despite softer sales, home values remained relatively steady. The median sales price rose slightly month-over-month to $349,450 (+0.6%), though it still sits 2.1% below last year’s prices. The median price per square foot held firm at $198, unchanged from October and just 1% lower year-over-year.

Homes spent a median of 49 days on the market, the same as in October but 11.4% longer compared to last year—another sign that the market is cooling at a slow, steady pace.

On the supply side, active inventory dipped to 10,248 homes, down 5.7% from October and 6.8% compared to November 2024. New listings also fell sharply, with just 2,386 hitting the market—a 23.4% drop month-over-month and 16.8% down from last year. This tightening supply may help stabilize prices heading into early 2026.

Overall, November reflected a quieter, more balanced market with slower buyer urgency and fewer new homes coming online—patterns we expect to continue through the winter months.

Hashtags

Northeast Florida Housing Market Update — November 2025

The November 2025 housing market showed a noticeable seasonal slowdown, with both buyer activity and new inventory pulling back as we moved into the holiday months.

Closed sales dropped to 1,864, which is a 20.2% decrease from October and 4.6% lower than November 2024. Fewer buyers stepped into the market this month, which is typical for late fall.

Despite softer sales, home values remained relatively steady. The median sales price rose slightly month-over-month to $349,450 (+0.6%), though it still sits 2.1% below last year’s prices. The median price per square foot held firm at $198, unchanged from October and just 1% lower year-over-year.

Homes spent a median of 49 days on the market, the same as in October but 11.4% longer compared to last year—another sign that the market is cooling at a slow, steady pace.

On the supply side, active inventory dipped to 10,248 homes, down 5.7% from October and 6.8% compared to November 2024. New listings also fell sharply, with just 2,386 hitting the market—a 23.4% drop month-over-month and 16.8% down from last year. This tightening supply may help stabilize prices heading into early 2026.

Overall, November reflected a quieter, more balanced market with slower buyer urgency and fewer new homes coming online—patterns we expect to continue through the winter months.